The Case Against Bitcoin: Once a Radical Internet Currency, Now Just Collateral for Banks and a Useless Veblen Good

Built by heretics, hermits, dreamers and rebels -- but still "rat poison squared"?

NB: Readers seeing this post on their email may see a truncated version. I will concede that it is a little long. The full version is always available on Substack.

“Wherever the institution of private property is found, the economic process bears the character of a struggle between men for the possession of goods.”

— Thorstein Veblen, The Theory of the Leisure Class, 1899

Scruffy, with an unkempt moustache, and often found with safety pins holding up his unwashed clothes, Thorstein Veblen was not the courtly man about town that the successful economists of his era had been.

He was an outcast. A sceptic. Utterly disdainful of organised religion, when most of the major economic institutions in America were funded by the church, and explicitly to educate Protestants, he struggled desperately to get his ideas noticed.

His manner didn't help.

He was reportedly sarcastic with everyone, prone to engaging strangers in bizarre practical jokes — like the time he borrowed a bag from a farmer only to return it with a bees nest inside — and had the overall air of a man who was “a mass of eccentricities”, as one biographer kindly put it.

Born into a tiny, communal Norwegian-émigré farming community in Wisconsin, Veblen was unemployed for seven years after graduating from Carleton, the small college near his home, but he eventually found a position at the University of Chicago. His colleagues found him “remote, aloof, disinterested…a flouter of convention.”

“He gave all his students the same grade, regardless of their work,” they said.

Rather than entertain guests, he would prefer to sit for hours in silence.

He refused to have a telephone, and saw no sense in making his bed.

“He allowed the dishes to accumulate until this cupboard was bare and then washed the whole messy heap by turning the hose on them.”

If this was Withnail and I, one might say to him: “You haven’t slept in 60 hours. You’re in no state to tackle it. There are things in there. There’s a teabag growing.”

Crucially, in the hunt for a potentially heroic outsider figure, Thorstein Bunde Veblen was not unkind, and not without a sense of humour.

When one student needed a higher mark to qualify for a scholarship, Veblen gladly changed a C to an A.

After he split up with his wife Ellen in 1909, Veblen took in four lodgers to his country house in Stanford, Connecticut.

They comprised two male undergraduates — who lived rent free, as long as they looked after the cows, chickens and horses — and a Das Kapital-obsessed housekeeper called Mrs Wilson, along with her daughter Virginia.

One day, the young girl, saw ‘T.B’ on a letter addressed to Thorstein, and asked him what the initials stood for.

He said: “Teddy Bear.”

Virginia forever referred to him that way. No one else would dare.

The Goodness of Goods

For a man so evidently untroubled by outward appearance, it is no surprise that his two major leaps forward in understanding were: why exactly humans love what we love; and why we display those things to others, in search of admiration, respect or approval.

The first was the calling card of the Victorian age: what Veblen coined as “conspicuous consumption”.

Today, we might call this peacocking, showing off, or wasting money on whims, to show it means nothing. What’s that you say? A wine bill comparable to the GDP of a small West African nation? Bring it here! Mere frippery!

The second really bold idea, one that took hold in early 1900s society*, was the notion of a Veblen Good.

This is a good in the way of goods and services, rather than a good thing or a bad thing.

The opposite: those prosaic, everyday, ‘normal goods’ that are interchangeable, and are things that usually see more demand as they get cheaper.

A household staple, like washing up liquid, would be in this category.

While Thorstein was evidently a stranger to washing up liquid, these ‘normal goods’ remain to the rest of us necessary purchases, requiring so little energy to consider that they just slip into the background.

But the idea of an item prized for its scarcity — not for the quantity that could be achieved for the lowest possible effort — broke ground because it ran contrary to the dominant economic orthodoxy of the time: that people bought goods according to the utility they provided.

Hearing this, one wonders whether orthodox economists ever went out into the world and actually met people.

Growing up the son of Norwegian farmers, Veblen was not a party to the lavish lifestyles of those he found at university, either in Chicago or among the WASP-ish elites at Cornell.

And at Carleton college, he came under the influence of John Bates Clark. Clark impressed on him to reject the idea of a man as a self-interested homo economicus, as put forward by Adam Smith in The Wealth of Nations**.

Instead, Veblen came to see people as fundamentally social animals conditioned by their exposure to institutions.

The Veblen Good proposed an object of desire, for which demand rises as the price rises.

To put it another way, demand for these things increases as their rarity, or scarcity, increases.

You might consider a Veblen Good a white elephant, if that elephant was also lacquered in gold and abstrusely expensive. An emblem of the distasteful ‘winning at life’ Instagram mentality. Vulgar and unhelpful, some might say.

Examples of Veblen Goods could include: precious metals, high-end fashion, a Rolex watch or a Fabergé egg.

Inflammatory and outrageous

I will offer you an example. I am a bit like Thorstein Veblen, in that I am often scruffy, and I buy most of my clothes from charity shops. For any of my American friends out there, the analogue is thrift stores — but the money I spend in charity shops goes back into the community through social projects organised by these charities, largely to help people who are down on their luck or need a hand.

(By the way, if this is your first time here: hello! I'm Tom. It's nice to meet you. I’m a writer and researcher, and sometimes a journalist, and the things that most intrigue me are behavioural economics and the human condition at large.)

The jeans I’m wearing while I write this article cost £4 from Oxfam, just down the road from where I live in Manchester.

These cheap trousers do exactly the same job as this artist-designed, curated and one-of-a-kind £4,200 pair by Harvey Nichols: that is, to keep my legs warm, and allow me to leave the house without being arrested.

The £4,200 pair does not do that job 1,000 times better than my £4 pair. The extra £4,196 is the premium people are willing to pay for unspoken soft power gained from owning an exclusive or scarce product.

The name of these jeans: Proleta Re Art, is a not-very-subtle nod to “proletariat”, the lowest class of citizens in ancient Rome, more currently used to describe working-class people, with reference to Karl Marx. A £4,200 pair of jeans is inflammatory enough without the need for a deliberate snub to us poor downtrodden masses who can’t afford them.

But the desire to own scarce things — a David Hockney original, a signed first edition Agatha Christie, rare Pokemon cards, a house with turrets — appears universal and unconstrained among the general population.

It just seems to be something that humans are really keen on.

And this sardonic hermit, this unwashed joker, Thorstein Veblen, with his messy moustache and his unwashed dishes, who spent his days concerned not with bond yields or trade deficits, but the outward, human, social aspect of economics, shone a light on an unnamed but pervasive phenomenon.

The question I want to ask is this.

Did Veblen, the outsider, the rebel, the sceptic, coin the phrase that now describes the ultimate outsider asset — Bitcoin?

Bitcoin promised so much, but has become an international lightning-rod for scorn. The common argument is that it is an unproductive, wasteful asset.

I would add that in its wider adoption (and institutionalisation) it has been effectively neutered by the system it sought to disrupt.

In becoming primarily an investable asset, it certainly appears to have divorced from its original intent: from the currency of the internet, to a digital-only improvement on gold.

So let’s look into it.

Bitcoin is not a currency any more

The Bitcoin whitepaper — which I would urge anyone to read — it’s only 9 pages long (for a work of groundbreaking supply-demand economics, game theory and computer science, this is quite astonishingly concise), and introduces: “a purely peer to peer version of electronic cash that would allow online payments to be sent from one party to another without going through a financial institution”.

It promises an anti-establishment, radical, outsider system to circumvent powerful middlemen and put agency, and control of private property, into the hands of normal, everyday people.

Its value can not be inflated away or debased — unlike fiat currencies controlled by central banks — because its supply schedule is set out in advance.

Today, 11 March 2024, 900 new Bitcoins a day are sent to miners for their work in processing blocks of transactions and keeping everything neatly organised and tracking who owns what. After 15 April 2024, that number will drop to 450 Bitcoins a day.

93% of all the Bitcoin that will ever be in circulation already exist, and only 1.5m BTC remain to be distributed over the next 115 years or so.

The reason why debasing a currency is so bad is that you inflate away value.

Increase the money supply, and everyone has more. But those people are chasing the same amount of goods and services.

“Debased” originally meant introducing small amounts of base metals, such as iron, into a currency supply — like eking out soup by adding more water.

Even the Romans, who were among the first societies to use gold coins as a means of exchange, gradually debased their currency to fund their expansion, to try to get more cross-border money out of the stock of precious metals they held.

On first reading, this ‘Bitcoin’ malarkey seems like a rather alien smashing-together of a bunch of complex mathematical concepts and internet-based technologies including public-private key cryptography, distributed networking, and game theory.

But it’s not difficult to see why the idea caught on.

There is nothing so powerful as an idea whose time has come.***

Launched by Satoshi Nakamoto in January 2009, Bitcoin certainly arrived at a time when faith in the banking system was at an all time low.

Public trust in the centralised institutions to whom we outsource money management had dropped faster than a fridge being pushed off the top of a tower block.

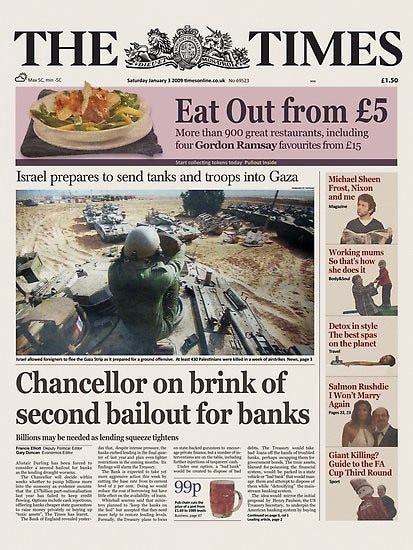

Encoded in the genesis (first) block of the Bitcoin blockchain are a message unlike any other of the hundreds of thousands of blocks that came after it: the words of a headline from The Times: “Chancellor on brink of second bailout for banks.”

A month later, Satoshi invited readers to try out this new currency model in a blog post on P2P Foundation:

“I’ve developed a new open-source P2P e-cash system called Bitcoin. It’s completely decentralized, with no central server or trusted parties, because everything is based on crypto proof instead of trust.”

Users of this Bitcoin currency would not have to trust that a small set of benevolent overlords would organise the system fairly, and keep their data and privacy safe, because the maths would prove it irrefutably.

And now for the kicker: “The root problem with conventional currency is all the trust that’s required to make it work.

“The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve.”

The post continues: “Before strong encryption, users had to rely on password protection to secure their files, placing trust in the system administrator to keep their information private. Privacy could always be overridden by the admin at the behest of his superiors. Then strong encryption became available, and trust was no longer required, no matter what.

“It’s time we had the same thing for money. With e-currency based on cryptographic proof, without the need to trust a third party middleman, money can be secure, and transactions effortless.”

If it reads like a manifesto, Satoshi always had (has?) that way about (him/her/them?) in (his/her/their?) writing.****

What Bitcoin did that was actually new

Many people had attempted to create secure peer-to-peer payment systems before, using the power of encrypted messaging. In 1983, the American cryptographer David Chaum created the concept of using ‘blind’ signatures as a way to create anonymous electronic cash.

In the late 1990s the Chinese-American computer scientist Wei Dai, who some suspect may be Satoshi Nakamoto, moved things forward when he proposed b-money. This was only theoretical, and was never released to the public, and so its influence was limited, but it did inspire Bitcoin, it seems.

Dai said to make a digital only currency work properly, the network of computers supporting it should carry out some kind of computational work, and the community should verify this work using a collective online ledger.

It also said that those processing transactions — what become Bitcoin miners — should be rewarded for that input, and this is the incentive mechanism of the block reward, paid in Bitcoins.

So Bitcoin was just the first technology of its kind to successfully combine a set of three key ideas and technologies.

Giving a network of computers, all running the Bitcoin software, an incentive to process transactions.

Forcing those who process transactions to show a ‘Proof of Work’, solving the previous intractable ‘double spend’ problem, proving that people had the Bitcoins they wanted to spend, without having to rely on a central authority to confirm it.

Using public-private key cryptography to make transactions secure

So you have a new type of system of record keeping, and you pay people in Bitcoin to keep it secure, and then you move on to the next day, and the next day.

Anyone who wanted to, and was willing to learn how it worked — could go into the code and see that Bitcoin was working as intended, its distribution was fair, and that it conformed to the rules that were set out.

But as we would find over the next decade and a half, the unintended consequence of creating the first example of digital-only, mathematically provable scarcity could be the exact thing that relegates Bitcoin to a museum piece.

Scale is good for you

In the 15 or so years since January 2009, Bitcoin developers have been so ideologically focused on security, that scalability — how quickly it could grow to be able to process billions of financial transactions a day — is still its largest unsolved problem.

By 2017, one set of developers, let’s call them the Blue Team, wanted Bitcoin to meet its promise of a being a globally available, internet-based fast-settlement payment system.

But another set of developers, let’s call them the Red Team, disagreed.

If you want scalability, they said, you’re going to have to wait for us to build this additional technology on top of Bitcoin, called the Lightning Network, that works on fundamentally different principles.

That peer-to-peer payment system, has still not taken off in the last seven years, and only accounts for around $332m (0.03%) of the $9bn of Bitcoin sent back and forth every day.

The disagreements were so intense that the Red Team went one way, into Bitcoin, and the Blue Team splintered, taking some of the transaction-processing computers with them, to start their own branch of the blockchain, which is now called Bitcoin Cash.

There is no doubt that the Bitcoin blockchain is secure. It works. It has near 100% uptime over the last 1.5 decades despite none of the miners (the computers who process transactions) having to know or trust one another. The Bitcoin blockchain has never been hacked. It is functionally impossible to counterfeit a unit of this currency.

For example, it would cost $87.6m a day for you to rent the computing power necessary to go back to the beginning of the Bitcoin blockchain and begin the process of reorganising all the blocks perfectly, so that no-one noticed, to assign yourself free Bitcoin. Given that the chain is monitored constantly, such an attack is implausible at best.

So — Is Bitcoin a Veblen Good?

If we track trading volume, that’s the amount of Bitcoin that changes hands between buyers and sellers on a given day, we can see quite clearly that demand for Bitcoin rises as its price rises.

The below chart looks at the period from 2015 onwards, when Bitcoin started becoming widely traded.

Just a note on this one, a standard price scale on the left hand side of the chart would normally show the same spaces between numbers as the same increments - from $0 to $10 to $20 to $30 to $40.

A logarithmic (log) scale uses those same spaces to show increases of a factor of ten between the numbers - from $800 to $8k to $80k. It’s usually used to show a very big range of numbers, like the increase in the Bitcoin price over the last 10 years, to fit it neatly onto one chart.

But for a currency to become mainstream, it has to have velocity.

It has to be used. It has to move from one place to another and be a readily available means of exchange for goods.

Velocity when it refers to money, means the number of times in a year that one unit of currency gets spent on goods and services.

Today, to work out the velocity of national money, like dollars or pounds, you take a country’s GDP and divide it by the total money supply.*****

For example, if the velocity of a US dollar is two, then every dollar in that economy gets used twice in a year.

My argument is that Bitcoin does not move enough, does not have enough velocity, to be considered a currency, and as such has defaulted to being a Veblen Good.

As the Cronut flies

Let’s consider another scarce, desirable Veblen Good of recent times — the Cronut.

This delicious pastry (I assume, never having got close to ever getting one, despite waiting in line in New York for 40 minutes before giving up and going to the pub), was created and trademarked in 2013 by chef Dominique Ansel.

In its own way, it is a radical smashing-together of the recognisable architecture of a doughnut with croissant-like layers of pastry.

Almost immediately after its debut, at $5 for a couple of bites of heaven at Ansel’s Soho bakery, supplies sold out. And that supply never scaled up to meet demand.

As its scarcity increased, demand increased, and we saw people paying vastly more than the cost of the delicacy for a spot in line.

Ditto: studies show that people are willing to wait far longer for something, and attach more intrinsic value to something, if it is something that others in their peer group find attractive. We see a line, and we assume that there is something scarce and valuable at the end of it that only a few ‘in the know’ people are going to be able to get.

There was some premium attached to Cronuts, because a secondary black market swiftly appeared, with enterprising buyers supplementing their insane Manhattan rents by reselling Cronuts on Craigslist at four or five times their sale price.

But there was no monetary or collateral premium on this warm and flaky delight.

As nice as a Cronut is, I can’t take it to a bank and use it as backing for a loan. Because it does not fulfil the other obligations that money must fulfil.

It is not durable: it will go mouldy in less than a week, even in an hermetically-sealed bank vault.

It is also not fungible: one unit is not the same as any other unit. One Cronut on a tray could be a little burned, or another could have a gram or two more butter in it, so you can’t standardise the price of other assets relative to one exact cronut. But with Bitcoin you can.

Bad money drives out good money

Personally, I can’t remember the last time I actually spent Bitcoin.

My logic is: it doesn’t make much sense to let go of an asset that rises in price relative to the cost of normal goods and services over time.

And whatever you think of Bitcoin, the fact is that its exchange rate against the US dollar has risen from $0, to $5, to $200, to $3,000 to more than $70,000 at time of writing.

There’s a description of this exact phenomenon called ‘Gresham’s Law’******., named after the 16th-century merchant and financier Sir Thomas Gresham. It states that ‘bad money drives out good money’.

This observable practice is that people prefer to spend less valuable money (bad money) in exchange for stuff they want and need on a daily basis, while saving or holding onto the more valuable money (good money).

In Gresham’s day, the less valuable money would be a national currency, while ‘good money’ would be gold.

So ‘bad money’, (which there is no major benefit to holding onto), circulates, while ‘good money’ (which may appreciate as a store of value) gets stuffed under mattresses, in a digital wallet, or locked in a safe somewhere alongside property deeds, a passport and a .45 handgun.

And most internet buyers and sellers seem to agree. The use of Bitcoin as a common day to day value transfer mechanism is not increasing, except among financial intermediaries like banks.

There is also the not-inconsiderable matter of transparency with Bitcoin transactions, which are now so widely tracked by the likes of Elliptic, Chainalysis and various law enforcement agencies that it doesn’t make sense for anyone wishing to remain anonymous to use Bitcoin.

Say, for example, you took a trip on to the dark web, to purchase some goods that are not technically legal in the place where you live. At one time, until around 2015, Bitcoin would be the currency demanded by the seller.

But as Bitcoin became less a currency and more a store of value, this function has been supplanted by other cryptocurrencies.

Monero (XMR) uses a swathe of alternative technologies not used on Bitcoin, like ring signatures and one-use-only stealth addresses, to deliberately conceal where coins came from, where they are going to, and how much was sent.

So now Monero reigns as the preferred non-sovereign currency for undertaking illicit transactions peer-to-peer: one of whom has an item, and the other of whom wants that item, and neither wants to know or meet the other.

Online, that is. Out in the concrete world, government-issued cash is still king when it comes to anonymous hand-to-hand payments.

37% of Bitcoin does not move

What Satoshi did not reckon on, it seems, is the strength of the desire for humans to possess something scarce, and the fact as scarcity increases, the rampant craving among a population also increases.

This is the narrative of Bitcoin as ‘digital gold’.

While around 4.2 million (20%, worth ~£220bn) of the total 21 million BTC supply is provably lost — stuck in wallets with forgotten passwords or on an old laptop accidentally thrown into a Welsh recycling dump, there is still the matter of the other 16 million or so Bitcoins out there in circulation.

Of those 16 million Bitcoin, 6 million (37%) have not moved in the last five years.

To prove this, we can use a type of analysis where we go into the Bitcoin records and look at the ‘age’ of coins — and when they were last moved between wallets.

This is called “on-chain analysis”. It is possible, because all of Bitcoin’s records of transactions are public.

That’s not to say on-chain analysis is easy. It takes ages, and you have to apply some machine learning if you’re doing it for a living, otherwise you’d grow old and die while slaving over a spreadsheet.

Still, digital assets that do move — that have appreciable velocity — that are exchanged for goods and services, either on the internet or out there in the real world, to pay my freelance friend to design the upcoming Charting Futures website, or to buy coffee in Buenos Aires, I would say are currencies.

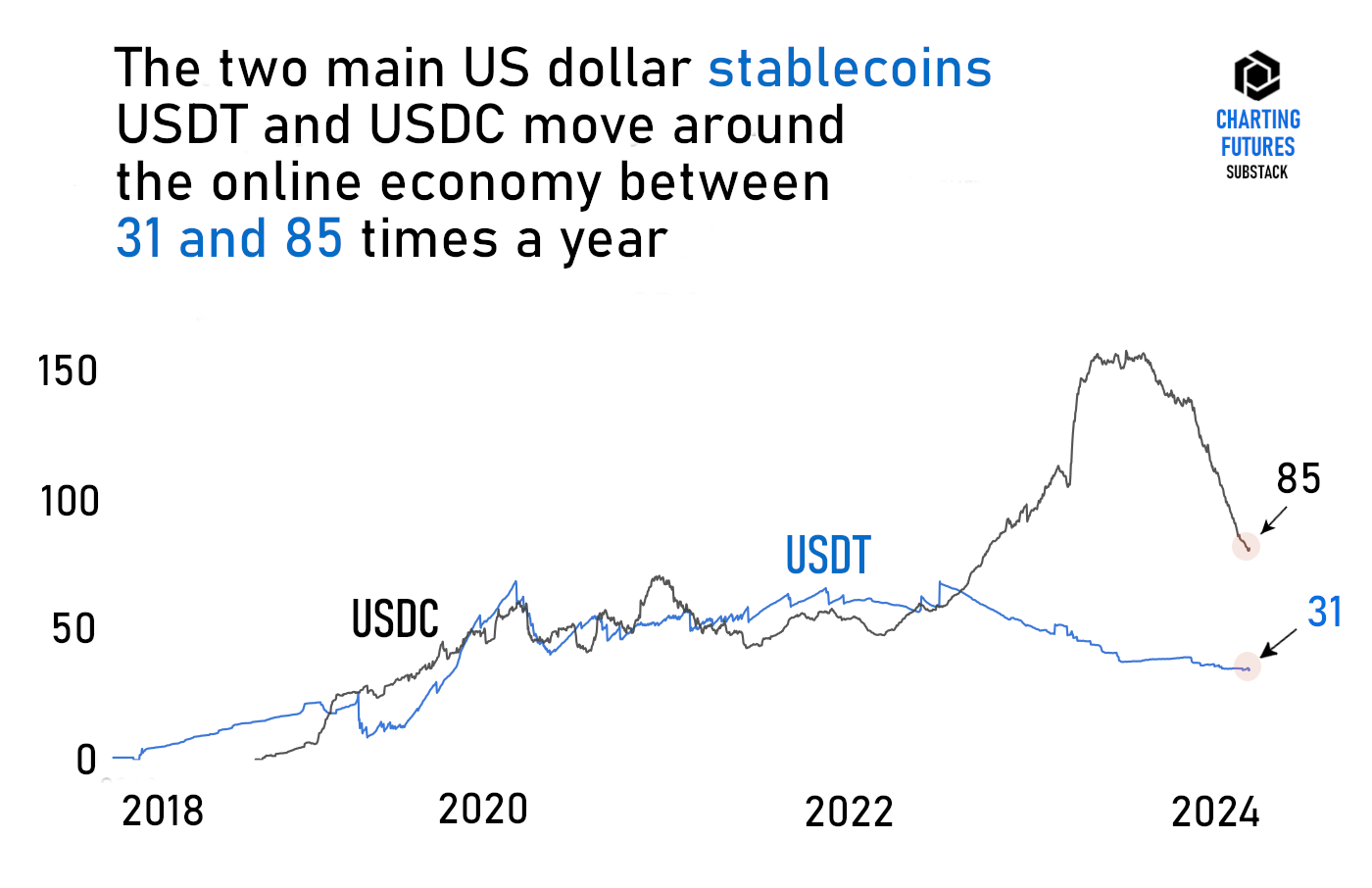

I can do this with US dollar stablecoins, the two largest of which are USDT, and USDC. These are currencies which have their transactions made final not by banks and their silo’d ledgers, but by a globally available, transparent and secure network checkable anywhere at any time. USDC is issued by Circle, a San Francisco-based tech company. It has $30bn of USDC in circulation, with each unit valued at $1.

Its core function and use case is to keep the value of a USDC at $1. By being available and transactable 24 hours a day, thanks to the Ethereum blockchain the program runs on, it does the same job as a normal dollar, only with 80 times more velocity.

The supply is backed (meaning it is linked to something with value out there in the non-online world) by US dollars and Treasuries that Circle has bought and holds on its balance sheet. If I have 1 USDC, I will always be able to convert it into 1 USD.

I was very surprised by just how much more velocity there is in US dollar stablecoins than for ‘paper’ dollars. But it’s doesn’t seem to be a mistake.

As this March 2023 paper in the Journal of International Money and Finance says:, the data “implies a daily USD velocity of an order of magnitude smaller than stablecoin velocities. A takeaway is that stablecoins are intensively used as vehicle currencies.”

Collateral Damage

To get back to the case in point, Veblen Goods tend to be things which hold worth, globally, over a long period of time, and are recognised by the majority of people who encounter them, to be scarce, and hence valuable.

Both a forgotten Rembrandt locked in a Swiss bank vault and Bitcoin, are scarce, but only Bitcoin is provably so, given that we can see how much of it is moving around at all times, and of the two it is only impossible to counterfeit a Bitcoin.

The other difference is that Bitcoin is a digital artefact native to the internet that can be liquidated anywhere in the world, within a couple of hours, 24/7, and not just between daylight hours on a weekday (and certainly not on a holiday) whenever traders decide to show up for work at a stock exchange or an auction house.

Bitcoin may still be a Veblen Good. But it is one that can be turned into cash faster than anything else.

As such, its main use now is likely to be how other highly liquid instruments are used: as collateral pledged by banks so they can lend and borrow against one another.

In its early days, when only six people knew what Bitcoin was, knowing that it had the properties of a new form of money wasn’t actually very useful, because only those six people could use Bitcoin as a means of exchange. But as it has gradually grown, and become steadily adopted by a laundry list of financial insiders, from CEOs to the head of the world’s richest investment banks.

Warren Buffett — worth noting because you have to respect a man who sticks to his principles — still thinks it is “rat poison squared”.

In 2016, one of the major moves towards Bitcoin as collateral happened. It got a reference rate. This is a once-a-day single source of truth price of Bitcoin via the Chicago Mercantile Exchange (CME). CME was originally the place where corn and soy and wheat futures contracts were settled, but has grown to become one of the largest derivatives exchanges in the world.

As Payal Shah, CME’s director of equity research, said on the Wolf of All Streets podcast a few years back: “Back then the price on all different spot exchanges was hugely varied. There wasn’t a point that we as a financial marketplace could point to and say: ‘This is the price of Bitcoin.’

With CME the centralised authority, now imbued with the old-world trust of one irrefutable number, and settling to transactors in fiat cash, Bitcoin “just plugs and plays in the same way that every other futures contract does. So really it’s exactly the same as trading the S&P 500 or gold,” Shah said.

And so Bitcoin became a collateral asset like anything else. Trading on a known entity like CME was done so “institutions could take that first step,” said Shah. “They don’t need to handle the underlying [Bitcoin] and they don’t need to know the intricacies of the network. Risk is mitigated, because we are the buyer for every seller and the seller for every buyer.”

And so Bitcoin was folded into the system.

Those that accept Bitcoin so readily now are the ones that directly profit from it as a tradeable asset. Just as Sam Bankman-Fried, of FTX infamy, admitted he knew nothing about blockchain, just that crypto was a desirable asset that could be traded.

His main wheeze was to profit from scalping the price difference for Bitcoin in South Korea (the ‘kimchi premium’), and the price it traded for in the US.

The world’s richest asset manager BlackRock now pulls in management fees every time market makers buy Bitcoin on an exchange somewhere and send it to their newly-launched Bitcoin ETF.

Hardly outsider, is it?

Why does gold get a free pass?

So — if Bitcoin is no longer a currency, nor a technology platform that people are developing cool and interesting new things on, should it be dismissed? Should nations (like China did en masse in 2020), send in the cops to shut down Bitcoin miner’s computers?

One point to explore here is that: in the modern era, 90% of gold’s value comes not from its use in industry, nor its use as a currency, but its uses as a Veblen Good, and as collateral.

And just because gold got here first, should it have an automatic right to squat in this section, even though its best attributes are improved upon in every way by Bitcoin?

Gold has a total market value of $10 trillion. Bitcoin has a total market value of about $2 trillion.

Because only 10% of gold is used in industry — in plating connectors and high-frequency conductors — that implies a market price of £160/oz ($200/oz) for gold.

But the monetary premium for the other 90% — the additional value added on top of this figure, because gold can be used as money — is worth $9 trillion.

And that comes from its ability to be used in soft power: as a status symbol in gold jewellery, as Veblen Good, and in investments, as collateral for obtaining loans.

But gold mining is one of the most destructive industries on earth. Quite apart from digging flipping great holes in the ground, there is the electricity needed to extract it, the diesel-powered trucks needed to take the ore from the mines for processing, and the fact that, as environmental pressure group Earthworks notes:

“It can displace communities, contaminate drinking water, hurt workers, and destroy pristine environments. It pollutes water and land with mercury and cyanide, endangering the health of people and ecosystems. Producing gold for one wedding ring alone generates 20 tons of waste.

“Gold mining can have devastating effects on nearby water resources. Toxic mine waste contains as many as three dozen dangerous chemicals including:

arsenic

lead

mercury

petroleum byproducts

acids

cyanide

“Mining companies around the world routinely dump toxic waste into rivers, lakes, streams and oceans – our research has shown 180 million tonnes of such waste annually. But even if they do not, such toxins often contaminate waterways when infrastructure such as tailings dams, which holds mine waste, fail.”

Gold may have been used as money and collateral for thousands of years, but its emergence as an investable asset only really appeared for the vast majority of us in the 1970s.

In 1933 it was made illegal for private citizens in the US to hold gold in the form of coins or bullion. This was only repealed in 1974, under President Gerald Ford.

Today we have the World Gold Council as an incredibly well-funded PR machine to tell us that demand for gold is increasing ad infinitum.

There is no World Bitcoin Council doing the same thing. Not yet, anyway.

If you are going to be critical of Bitcoin’s electricity use — I mean, really — be critical of the amount of electricity, petrol, natural resources, water and everything else it takes to get gold out of the ground.

To argue anything else would be intellectually dishonest.

Bitcoin bad, Veblen Good?

In sum, the narrative and major use of Bitcoin as digital gold, rather than a peer-to-peer currency, seems so prevalent now that it will be difficult to turn the clock (or block) back.

Does this mean it should not have a right to exist?

Not by my reckoning. Not if you don’t apply the same argument to shutting down gold miners, or raiding Swiss bank vaults.

Does this mean it will not increase in value relative to national currencies in the future?

Nobody knows for sure, but probably not, knowing what we know about Veblen Goods.

Does this mean the character of Bitcoin will not change in future?

I don’t think so. There are still some interesting experiments being done on Bitcoin’s code.

It’s just not as malleable as Ethereum. It’s not designed to be a platform that anyone can access with a digital wallet, and then program any function they want onto a token.

But one example of potential interesting routes forward are the work done by Casey Rodarmour, which creates individual, uniquely-scarce NFT-like objects inside the smallest unit of a Bitcoin, the satoshi.

It’s like taking all the leftover 1p coins in the world and drawing funny pictures on them, effectively. If you are concerned that taking this many pence, or cents, out of circulation could be a problem in future, it is worth noting that Bitcoin is divisible to eight decimal places.

When the total supply of 21 million Bitcoin is reached sometime in the early 2100s, 2.1 quadrillion satoshis will have been mined into circulation.

There are also the experiments by John Light, to see whether Bitcoin, like Ethereum, could take advantage of rollups, which are a way to batch transactions and processes them in a separate program, so as to take computational pressure off the main chain (basically, to speed up how quickly transactions can be settled, and final).

He also has some fun-looking work on the privacy-protecting features of these things called zero-knowledge proofs (there is a great explainer in five levels of difficulty: child, teenager, college student, grad student, professor by Amit Sahai from UCLA here).

It’s a lot to take in. I’ve edited this post quite a lot of times. I will accept it is a little long. But editing out interesting ideas is like cutting your own limbs off, when you’re passionate about a topic.

And nothing creates passion like a novel upstart who disrupts the status quo, unapologetically rails against the unrestrained excess of those who purport to rule with moral authority, and brings something truly new into the world.

The great Russian science fiction author, Yevgeny Zamayatin, of We fame, described true literature or art existing only “where it is created, not by diligent and trustworthy functionaries, but by madmen, hermits, heretics, dreamers, rebels and sceptics.”

Veblen was certainly one. Perhaps Satoshi was too.

And if you are at all interested in how economic realities are organised, you can’t deny that Bitcoin is fascinating.

Initially, it does tend to attract the weirdos and fringe elements of our world.

The unshaven cyberpunk, the Reddit-obsessed programmer, the radical End of The World insurance buyer. This total addressable market has gradually broadened out as Bitcoin has persisted, but it has taken more than a decade.

As for Bitcoin: despite having researched it for eight years, I’m still unsure. From a scarce resource-that's-provably-better-than-gold perspective, it feels uncomfortably likely that my descendants might be quite annoyed that I was here at the birth of a the world’s first provably scarce digital-only asset and I still didn't buy any.

But every investor, scruffy outsider, economist, user, rebel, hermit, dreamer or sceptic will have to decide for themselves.

End Creditors

*Even after the publication of The Theory of the Leisure Class, Veblen found little support, and despite its growing influence was even denied a raise to his meagre wage by the University of Chicago. I weep for public sector pay, I really do.

**That’s not to say The Wealth of Nations is not worth reading. As JK Galbraith wrote in his excellent 1987 book A History of Economics: The Past as the Present: “Wealth of Nations is a vast, disorderly treatise, rich in amusement and written in admirable prose but, with the Bible and Marx’s Capital, one of three books that the questionably literate feel they are allowed to cite without having read. Especially in Smith's case this is a grave loss."

And Galbraith’s own effort is a cracking read, too. It was from this that I learned the fabulous word ‘sinecure’: a cushy job, from which little work is expected but much financial benefit is derived.

Just learning this word put the idea in my head that I should really knuckle down and refocus my efforts on refining my sinecures.

*** I thought originally this quote was by the great French novelist Victor Hugo in his 1877 work The History of a Crime, but it turns out this is not the case. The closest match comes 30 years earlier, from an 1848 article by the French writer Emile Souvestre in a periodical called Two Worlds Review: “Or, dans toute question humaine, il y a quelque chose de plus puissant que la force, que le courage, que le génie même: c’est l’idée dont le temps est venu.” In translation, “Now, in every human question, there is something more powerful than strength, than courage, than genius itself: it is the idea whose time has come.”

****The fact that we still don't know Satoshi Nakamoto's identity is wild, to me. Which other inventors have managed to remain entirely anonymous, while their innovation spread like wildfire? They could be dead. Or if alive, and having amassed a multi-billion dollar fortune, extremely paranoid. Show me the man, and I’ll show you the crime, as the notorious head of the Soviet secret police, Lavretiy Beria, said in 1941.

*****You would think it would be quite easy for a central bank to know how much money supply there is, but this is one of the thorniest and most often debated questions in economics — what constitutes money — is it savings? bank loans? Economists quite often change their minds, like the US Federal Reserve did when it removed money market funds from their equation as recently as 2020.

I struggled to find the same publicly available data for UK GBP velocity — if anyone can find this buried somewhere in the Bank of England website please let me know in the comments — or you can email me at chartingfutures at gmail dot com. I am also not sure of the optimal velocity of a currency, if anyone has any data or thoughts on that.

******The astronomer, mathematician and stone-cold genius of Renaissance Europe, Nicholas Copernicus, described this same principle in 1526, in a paper written for the King of Poland, called Monetae cudendae ratio. It states that ‘debasement of the coin’ is one of the major reasons why great societies collapse.

There was recently a good “In Our Time” podcast (Melvyn Bragg) about Veblen and conspicuous consumption. Strangely bitcoin was never mentioned!

This article (though long!) is a real tour de force in terms of setting out where we are currently up to with bitcoin in very straightforward comprehensible terms. It is fascinating and slightly worrying to think that something so radical and revolutionary seems to have been neutered and disrupted by a number of factors, a mixture of greed and the power of the establishment and established ways of doing things. Made me think of parallels with Orwell’s Animal Farm..

An excellent read.